Wondering how to make the most of your small business tax deductions? If so, you’re not alone. Most small company owners are constantly searching for ways to keep costs under control and reduce their annual tax burden.

Luckily, there are plenty of creative tax deductions for small business you can claim to keep more of your hard-earned money! In this piece, we discuss how to report your tax deductions and what types of company expenses are eligible.

How do I report my tax deductions?

To report income and claim tax deductions as a small business owner, you need to fill out Form 1040 (including Schedule SE for Self-Employment Tax) and Schedule C (the “Profit or Loss from Business” attachment).

Essentially, the profit or loss you see in your Form 1040 calculations will be your total income for the year.

How do I know if I itemize my deductions?

If you’re wondering how to maximize tax deductions for your small business, then you need to understand the differences between standard and itemized deductions.

The first option (standard deductions) is easier from a formal standpoint. All you have to do is look up the applicable tax deduction amount on the IRS site and claim it on your 1040 form. As of 2023, the standard rates are:

- $13,850 for single taxpayers (or married individuals who decide to handle taxes separately)

- $27,700 for married couples, and

- $20,800 for heads of households.

While popular among taxpayers who work on employment contracts, standard deductions aren’t always the best option for small business owners. Why? If you know what types of business costs are eligible for tax deductions, you might save more money through itemizing.

So how do you know if it makes sense for you to itemize? Let’s run a quick simulation and assume you’re a single, self-employed individual. This would make you eligible for a standard $13,850 tax deduction. However, after adding up all your company-related expenses, you uncover that you’ve spent $15,450 on your business. The amount exceeds the standard tax deduction rate by $1,600, which means you’d save more money by itemizing.

That said, in order to itemize, you need to keep each invoice, receipt, and 1099 form from suppliers and contractors on file. These documents will make you eligible for your small business tax deductions.

How many deductions should I have on my taxes?

If you decide to itemize your company expenses, then the more, the better! That said, they must be both “ordinary” and “necessary”. The first term relates to expenses that are common and accepted for companies in the same line of business. Meanwhile, the IRS defines “necessary” expenditures as “helpful and appropriate”. The good news? A company cost doesn’t have to be indispensable to be greenlighted by the IRS – you just have to prove that it helped you operate your business better.

This means that an expense that is both “ordinary” and “necessary” can also be “creative”. Creative tax deductions for small business are the company costs that you might not initially think of while itemizing your deductions.

For example, if you’re a certified translator, some expenses that you’re likely to think of straight away would include tickets to industry conferences, online dictionaries, office supplies, and hardware. But you could also get more ‘creative’, and list travel expenses like subway tickets, dry cleaning, or home-office costs like the business part of your property tax or phone bills.

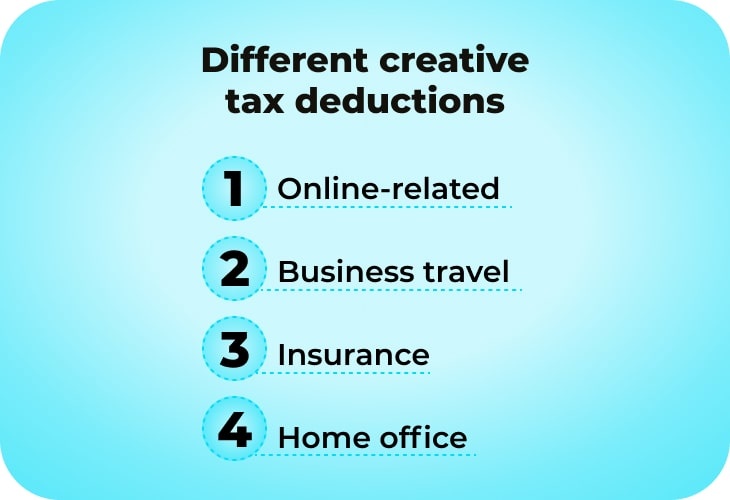

Ready to see the full list? Here are over 40 types of common, acceptable, and creative tax deductions for small business.

Online-related tax deductions

Here are some ways you can use your digital-related expenses to reduce your tax obligations.

Marketing spend

Getting the word out there about your business is certainly eligible for a tax write-off. The IRS lets you deduct the costs of marketing and advertisement that not only directly promote your business, but also help create brand awareness. For example, you can deduct a campaign that features your logo but encourages people to contribute to Doctors Without Borders or UNICEF. However, this doesn’t apply to ads taken out to influence legislators or endorse a political party.

Here are a few popular marketing collateral types you can deduct:

- Ads on Facebook, Instagram, and other social media platforms

- Search engine advertising

- Sponsored articles

- Podcast episode sponsorships

- Subscription to a marketing platform for small business – for example, one that lets you engage in lead nurturing or run email and text message campaigns.

Software and online tools

What programs or plug-ins do you pay for on an annual or monthly basis? Think of industry-specific tools (like SEO software if you’re a marketer) and general ones that help you in your daily operations.

Some types for you to consider include:

- Cloud platforms for file storage

- Accounting/invoicing software

- Video conferencing tools

- Online payment processing tools

- Subscriptions to premium plans (for example, Meta for Business or LinkedIn Premium)

- Microsoft Office, LibreOffice, or other paid suites.

Speaking of online tools, here’s a category that deserves a section of its own.

Website design and maintenance

Websites will always generate costs. These can be a couple hundred dollars if you’re just paying for the domain and hosting, or thousands if you’re using paid software and working with a designer or developer. In any case, it’s a very “promising” category for small business tax deductions.

Here are a few expenses that would qualify as ordinary and necessary:

- Domain renewals and domain name parking. This basically means buying a domain name with the intention of using it further down the line, rather than creating a site for it immediately, to stake your claim to a valuable digital asset related to your brand.

- Hosting and subscriptions to website builders like WordPress or Squarespace

- Cybersecurity – for example, SSL certificates cost and premium extensions like firewall

- Paid plug-ins, like SEO optimization tools

- Website design software like Sketch or InVision

- Monthly retainers from design, SEO, and software development contractors.

Business travel tax deductions

If you travel for work, then you might be able to deduct quite a few associated costs.

What qualifies as business travel?

To qualify travel as a business cost, you need to be away for more than a full day’s work (i.e., need to rest or sleep away from home). Also, make sure that none of the expenses are “lavish, extravagant, or for personal purposes”. Using corporate travel agents can help streamline your travel planning and ensure compliance with tax regulations while managing expenses effectively. We discuss what qualifies for tax write-offs next.

What business travel expenses are tax deductible?

Here’s a non-exhaustive list of deductible costs for your business travels:

- Hotel, apartment, or other lodging expenses

- Shipping display, marketing collateral like company swag, or other items between your main place of business and temporary work location

- Business communication, for example, international calls

- Dry cleaning and laundry services

- Travel fares for bus, train, and airplane tickets, as well as car rentals

- Other means of transportation, for example, subway tickets or taxi fares for traveling between your hotel and off-site work destination

- Some meals (we discuss the exact conditions next)

- Tips for any of the services above.

Are meals while traveling for business tax deductible?

Yes, but from 2023 onward, you can only deduct 50% of the cost. This covers all of your own meals and any lunch or dinner you treat your customers to. Also, be careful when choosing the venue. You won’t be able to deduct a dime from anything that the IRS qualifies as too elegant and over-the-top.

There are only two types of food-related travel expenses that are still 100% tax deductible. These are:

- Food and drinks that you’re planning to give away (for example, during a conference or public event)

- Meals for you and your employees, provided that you’re working overtime.

Insurance tax deductions

This is another category that can help you lower your taxable income.

What insurance payments are tax deductible?

You can deduct taxes from any insurance that relates to your business and qualifies as both ordinary and necessary. So, you’re unlikely to face issues writing off any insurance required by your industry, contractual agreements, and state regulations.

Here are some of the deductible premiums:

- Insurance for losses resulting from natural disasters, theft, and similar circumstances.

- Life insurance for you and any of your employees (provided that you’re not the main beneficiary)

- State unemployment insurance plans

- Malpractice insurance

- Vehicle insurance (if you use the vehicle for both personal and business purposes, you can deduct only part of the cost).

If you run a sole proprietorship, you might also be able to deduct health insurance for you and your family. However, these costs will be deducted from your income as an individual – not your company.

Is general liability insurance tax deductible?

Yes, general liability insurance also qualifies as an ordinary and necessary business expense.

Home office tax deductions

Work from home? Here are a few tax tips for small business owners who don’t commute to the office.

How much can you write off for a home office?

It all depends on how much space you take up to operate your business. Say you’re a fashion designer and converted the entire attic into your studio. It makes up about a quarter of your home’s total square footage. This means that you’d be able to deduct 25% of your total annual utility expenses.

What can a home-based business write off?

On top of utilities, you can also deduct the ‘business’ portion of your:

- Home insurance

- Internet and cell phone costs

- Casualty losses

- Property depreciation

- Rent (if you’re not the property owner)

- Mortgage interest

- Maintenance

- Real estate taxes.

What you can’t deduct are costs that are unrelated to your business. So, if you decide to renovate your living room and don’t use it for work, you won’t be able to deduct tax.

How to maximize tax deductions for your small business

As you can see, there are many ways you can reduce your tax obligations. Hopefully, after giving this piece a read, you’ve spotted a few options you weren’t previously aware of!

If you decide to itemize your tax deductions, make sure that they qualify as both necessary and ordinary. Also, keep track of all your receipts, invoices, and 1099s. When in doubt, refer to this article and the IRS site for a deeper dive.

Here’s to making the most of the upcoming tax season!