As a small business owner, the tax burden on your business income and taxable income can be crushing. The good news is that there are many tax deductions and loopholes you can use to avoid paying high personal taxes and slash your tax bill.

By taking advantage of write-offs, finding the best business structure, and making good use of tax-free plans, you can reduce your taxes and maximize the amount you get to keep. Consulting with a tax professional can help you navigate tax law and find even small business tax loopholes. Arm yourself with knowledge about little-known tax breaks for small business owners before you file your next tax return as a sole proprietor.

Tax loopholes for small businesses

Why hand over more than your fair share to the IRS? The tax code contains some perfectly legal loopholes that can help reduce your tax burden.

Here are a few to consider:

- Tax deductions for common business expenses like business meals, supplies, and home office costs. Keep good records and receipts to claim these deductions on your tax return.

- Tax-savvy business structures like limited liability companies allow you to take deductions for health insurance and other employee benefits. They also provide liability protection and the possibility of lower tax rates.

- Retirement plans like an IRA or 401(k) have tax deductible contributions, and the money in the account grows tax deferred. This helps you save for the future and lowers your taxable income today.

Consult with a tax professional to explore other options like depreciation deductions, business use of your vehicle, travel and entertainment expenses. They can advise you on reducing your taxes in a compliant way based on your unique situation.

Choose the right business structure to minimize taxes

One of the easiest ways to reduce your taxes is to choose the right business structure. Many small business owners form a sole proprietorship, because the paperwork is simpler. But this business structure has the highest tax rates.

A partnership, LLC, and corporation all offer varying tax benefits. If you form a partnership or limited liability company (LLC), your share of business income still flows through to your personal tax return, but you may qualify for some additional business deductions.

Forming a corporation provides the most tax benefits. Corporations pay taxes separately from their owners at lower corporate tax rates. You can also take advantage of more tax deductions like business meals, retirement plans, and home office expenses. However, corporations require more complex tax filings and record keeping.

The best approach is to consult with a tax professional to determine which structure fits your needs. They can help you take advantage of every tax deduction and loophole available under the tax law to slash your tax bill.

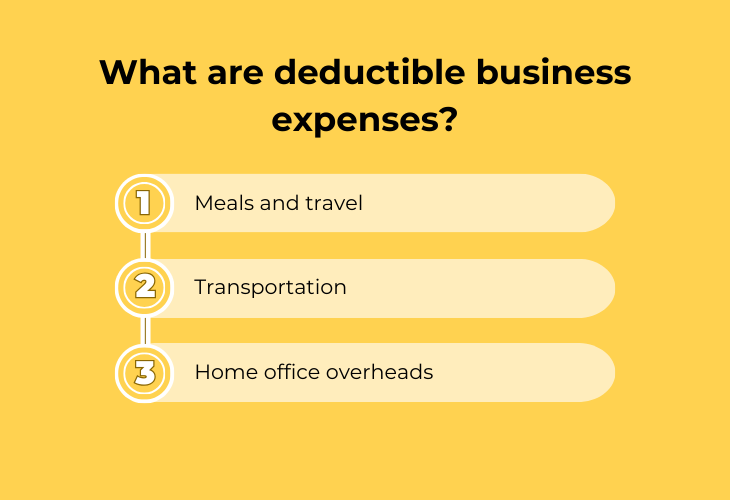

Reduce your taxable income with business expenses

The tax law allows you to deduct expenses incurred for business purposes, so track everything you spend on your business to take advantage of these tax deductions and reduce your tax burden. Here are some of the most common deductible business expenses.

Meals and travel

Keep records of any business meals, travel, or entertainment that has a clear business purpose. Even lunches with clients or dinners with colleagues can qualify as legitimate business expenses, as long as you’re using them for business purposes. Make sure to note the attendees and discussion topics.

Transportation

Does your business require the use of a vehicle? You may be able to deduct vehicle expenses like gas, insurance, repairs, and depreciation. Keep detailed mileage logs and records of expenses. Some business owners are able to deduct up to 100% of vehicle costs.

Home office overheads

Do you work from home? Claim the home office deduction for the portion of your home used exclusively for your business. This includes a percentage of utilities, insurance, repairs, and rent or mortgage interest. Many small business owners miss out on this lucrative deduction.

Other common business expenses include office supplies, professional services, and employee benefits. It’s best to sit down with your tax professional to determine what qualifies as a deductible business expense, based on your business type and tax status.

Contribute to retirement plans to lower your tax bill

Contributions you make to retirement plans like SEP IRAs, SIMPLE IRAs, and solo 401(k)s are tax deductible. That means the money you put in reduces your taxable income, so you avoid paying taxes on it now. And with lower taxable income, your business may drop into a lower tax bracket. These benefits apply to your own retirement plans, and those you contribute to for your employees.

Contributions to retirement plans benefit your business in two ways:

- Lower your business income and taxes now.

- Provide for your future and build wealth.

The money in the plans grows tax deferred until you withdraw it in retirement. Some plans even allow loans against the balance, which you pay interest on but the interest also goes back into your own account.

Here’s a brief overview of tax-deductible retirement plans:

A SEP IRA allows you to contribute up to 25% of your income or $57,000 for 2020, whichever is less.

A SIMPLE IRA permits contributions of up to $13,500 for those under 50, and $16,500 for those over 50.

A solo 401(k) lets you contribute up to $57,000 for those under 50, and $63,500 for those 50 and over.

As with any tax strategy, be sure to consult with a tax professional to determine which retirement plan is right for your small business and make the most of the tax deductions. Setting up a retirement plan may seem complicated, but the tax savings and peace of mind about your financial future make it worth the effort for small business owners.

Trying out the Augusta strategy

The Augusta principle allows you to avoid paying personal income tax on business income by setting up a limited liability company (LLC) or corporation. If you operate as a sole proprietorship or partnership, forming an LLC or corporation can lower your tax rate, because business income and expenses are separated from your personal tax return.

Your business’s taxable income is subject to the corporate tax rate, which is often lower. Any income you draw as salary or dividends from the business is then taxed at your personal tax rate, but it will be lower than your business’ overall taxable income.

To properly implement the Augusta strategy, you must keep good records to prove your business expenses are for a legitimate business purpose. Track things like:

- Business meals

- Office supplies

- Travel

- Rent

If done right, the Augusta strategy can help small business owners like yourself significantly reduce your taxes.

Snagging the QBI deduction for your taxes

The qualified business income deduction, or QBI deduction, is a tax break created specifically for small business owners like yourself. It allows you to deduct up to 20% of your business’s taxable income from your personal tax return, even if you’re a sole proprietor. This lowers your taxable income and tax rate, reducing the amount you owe in taxes.

To claim the QBI deduction, you must meet a few requirements:

- You must operate your business as a sole proprietor, partnership, S corporation, or limited liability company. C corporations do not qualify.

- You must have a legitimate business purpose for all business income and expenses reported on your tax return.

- Your taxable income must be below $160,700 for single filers, or $321,400 for joint filers, to qualify for the full 20% deduction.

- You’ll need to report your business income and expenses correctly on Schedule C, E, or F, and Form 1065 or 1120S. Then you can claim the QBI deduction on Form 1040.

The calculation can be complex, so it’s highly recommended to consult with a tax professional, to ensure you get the maximum deduction you’re entitled to.

Start shrinking your tax bill

The tax law contains many provisions to help small businesses. Do your homework and work with experts to take advantage of these legal loopholes so you can keep more of the money you earn and continue fueling your entrepreneurial passion. Paying less in taxes means more resources for growing your business.